Atal Pension Yojana Calculator 2026: Retirement planning often feels like a burden. We think we need lakhs of rupees to start. But what if you could secure a guaranteed monthly pension of ₹5,000 for the rest of your life by investing just the price of a cup of tea today?

Welcome to the Atal Pension Yojana (APY), the Government of India’s flagship social security scheme launched by Prime Minister Narendra Modi.

Designed primarily for the unorganized sector, APY promises a fixed pension to citizens aged 18 to 40 years. However, the contribution amount depends heavily on your entry age. A delay of just one year can increase your monthly payment significantly.

That is why we built the UsefulAITool Atal Pension Yojana Calculator.

Stop guessing. Use our free tool to find out exactly how much you need to invest today to get a worry-free retirement tomorrow.

What is Atal Pension Yojana (APY)?

The Atal Pension Yojana (APY) is a government-backed pension scheme administered by the PFRDA (Pension Fund Regulatory and Development Authority). It was introduced in the 2015-16 Budget to provide a safety net for workers who do not have a steady income or EPF benefits.

Key Highlights:

- Guaranteed Pension: You choose a pension slab of ₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000 per month.

- Government Guarantee: If the actual returns on investment are lower than the guaranteed pension, the Government of India funds the deficiency.

- Triple Benefit:

- Pension to Subscriber (You).

- Pension to Spouse (after your death).

- Return of Corpus to Nominee (after spouse’s death).

How to Use the APY Calculator

Our advanced calculator simplifies the complex APY charts provided by banks. Here is how to use it:

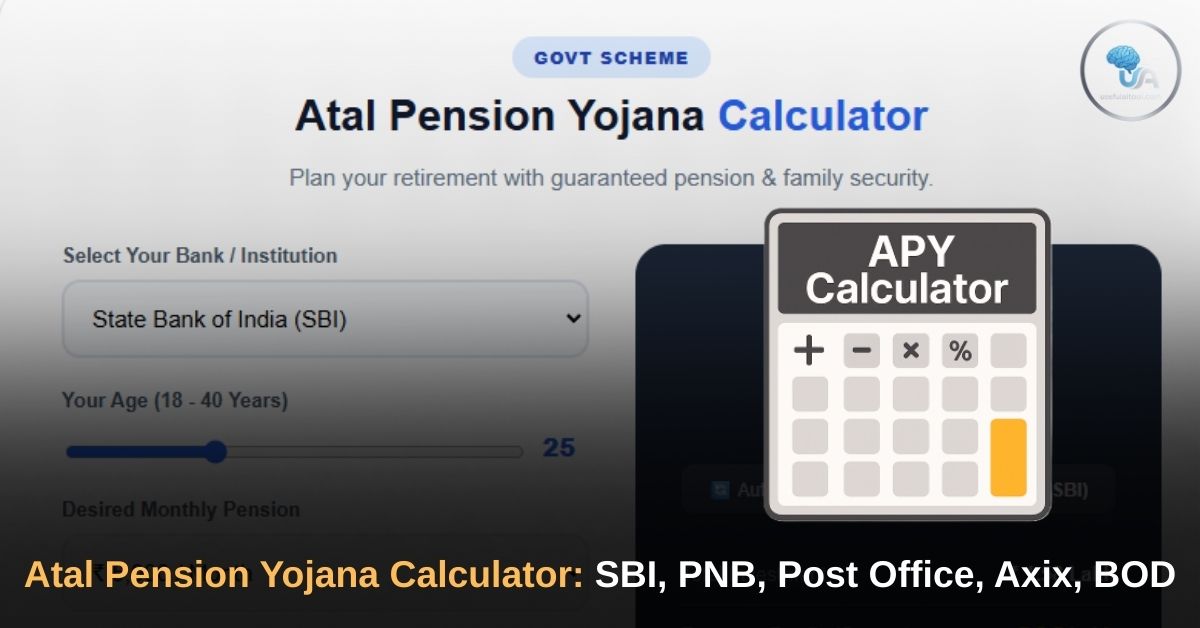

Atal Pension Yojana Calculator

Check Monthly Contribution for SBI, PNB, Post Office & More.

🚀 Profit: You pay 1.5L, Family gets 8.5L

Step 1: Enter Your Age

Move the slider to your current age. The scheme is open for people between 18 and 40 years.

- Note: You cannot join APY if you are older than 40.

Step 2: Select Desired Pension

Choose how much monthly pension you want after the age of 60. The options are ₹1,000, ₹2,000, ₹3,000, ₹4,000, and ₹5,000.

Step 3: Check Your Contribution

The calculator will instantly show you:

- Monthly Contribution: The amount to be auto-debited from your bank account.

- Total Investment: The total money you will pay until age 60.

- Corpus Return: The lump sum amount your nominee will get (e.g., ₹8.5 Lakhs for the ₹5,000 slab).

The “Hidden” Power of APY: Family Security

Most people think APY is just about their own pension. They miss the biggest benefit: Wealth Creation for the Family.

The APY structure is designed to support three generations. Let’s take the example of the highest slab (₹5,000 Pension):

- Subscriber (You): You receive ₹5,000/month from age 60 until death.

- Spouse (Husband/Wife): After your demise, your spouse automatically receives the SAME pension (₹5,000/month) for their lifetime.

- Nominee (Child): After the demise of both you and your spouse, the accumulated corpus of ₹8.5 Lakhs is returned to your nominee.

This makes APY not just a pension scheme, but a legacy plan for your children.

Atal Pension Yojana Contribution Chart (2026 Updated)

Your contribution amount is locked at the time of joining. If you join at 18, you pay less. If you join at 40, you pay more.

Here is a quick look at the monthly contribution for the popular ₹5,000 Pension Slab:

| Entry Age | Monthly Contribution | Total Years to Pay | Total Investment (Approx) | Return to Nominee |

| 18 Years | ₹ 210 | 42 Years | ₹ 1.05 Lakh | ₹ 8.5 Lakh |

| 25 Years | ₹ 376 | 35 Years | ₹ 1.58 Lakh | ₹ 8.5 Lakh |

| 30 Years | ₹ 577 | 30 Years | ₹ 2.07 Lakh | ₹ 8.5 Lakh |

| 35 Years | ₹ 902 | 25 Years | ₹ 2.70 Lakh | ₹ 8.5 Lakh |

| 39 Years | ₹ 1,318 | 21 Years | ₹ 3.32 Lakh | ₹ 8.5 Lakh |

Analysis: A person joining at 18 pays only ₹210/month. A person joining at 39 pays ₹1,318/month for the same benefit. Start Early!

Eligibility Criteria: Who Can Open an APY Account?

To apply for the Atal Pension Yojana, you must meet the following simple criteria:

- Citizenship: Must be an Indian citizen.

- Age Limit: Must be between 18 and 40 years of age.

- Bank Account: Must have a valid Savings Bank account (Post Office accounts are also valid).

- Mobile Number: Must be linked to the bank account for SMS alerts.

⚠️ Important Update (October 2022)

Income Tax Payers are NO LONGER Eligible.

If you are an income tax payer (i.e., your income exceeds the taxable limit and you file ITR), you cannot join APY starting from October 1, 2022. This move was made to target the scheme better towards the underprivileged and unorganized sectors.

Need More Financial Tools?

- Planning a Road Trip? Use our Fuel Cost Calculator to budget your travel expenses accurately.

- Want to Earn Extra Income? If you are planning to start a YouTube channel to supplement your pension, check our YouTube Income Calculator to see potential earnings.

- Content Creator? Use our YouTube Tag Extractor to rank your videos and grow faster.

Tax Benefits of Investing in APY

Even though tax payers can no longer join, existing members and those who are not tax payers (but might be in the future) enjoy excellent tax benefits under the Income Tax Act, 1961.

- Section 80CCD(1): Your contribution is eligible for tax deduction within the overall limit of ₹1.5 Lakh under Section 80C.

- Section 80CCD(1B): You can claim an additional deduction of up to ₹50,000 over and above the ₹1.5 Lakh limit. This is exclusive to NPS and APY subscribers.

APY vs. NPS vs. PPF: Which is Better?

Choosing a retirement fund can be confusing. Here is a quick comparison:

| Feature | APY (Atal Pension Yojana) | NPS (National Pension System) | PPF (Public Provident Fund) |

| Guarantee | 100% Govt Guaranteed Pension | Market Linked (Not Guaranteed) | Govt Guaranteed Interest |

| Returns | Fixed (₹1k – ₹5k) | High (8-12% expected) | Fixed (7.1% currently) |

| Risk | Zero Risk | Moderate to High Risk | Zero Risk |

| Who is it for? | Low Income / Unorganized | Corporate / High Income | Safe Investors |

Verdict: If you want peace of mind and a fixed income without worrying about stock market crashes, APY is the winner.

FAQs on Atal Pension Yojana Calculator

Q1: Can I exit the scheme before 60?

Voluntary exit is allowed, but not recommended. If you exit before 60, you will only get back your own contribution and the interest generated on it. The government’s co-contribution (if any) will be deducted. However, in case of death or terminal illness, the full corpus is returned.

Q2: Can I upgrade my pension amount later?

Yes. If you started with a ₹1,000 pension plan but now earn more, you can upgrade to the ₹5,000 slab. You will just have to pay the difference amount for the backdated period. This can be done once a year in April.

Q3: Is Aadhaar mandatory for APY?

While Aadhaar is not strictly mandatory for opening the account, it is highly recommended as the primary KYC document. It ensures seamless claim settlement for your spouse and nominee in the future.

Q4: Can I have two APY accounts?

No. One person can have only one APY account. This is linked to your PRAN (Permanent Retirement Account Number).

Conclusion: Don’t Wait for Tomorrow

Retirement planning is not about how much you earn; it is about how early you start.

As our calculator shows, starting at age 18 costs you less than a movie ticket per month. Waiting till 35 makes it five times more expensive.

Secure your future and your family’s legacy today. Visit your nearest bank or use Net Banking to enroll in Atal Pension Yojana.